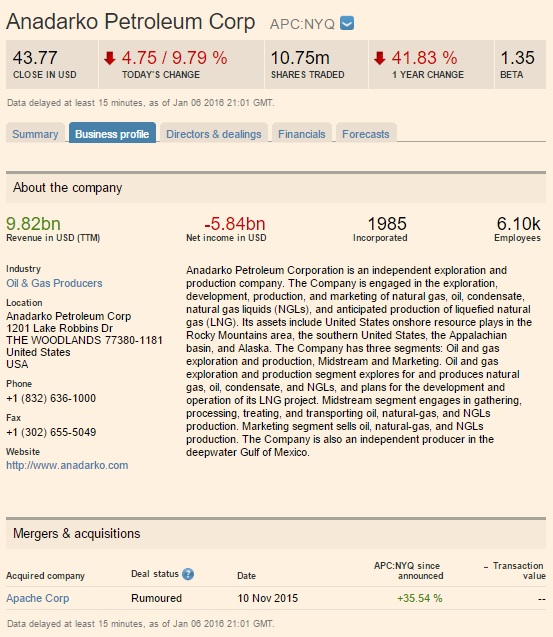

ANADARKO PETROLEUM CORP (APC)

43,77 USD

-9,79% | -4,75

06/01/2016 22:01

TheStreet.com - Jan 5, 2016

NEW YORK (TheStreet) -- Anadarko Petroleum Corp.(APC) stock closed lower by 1.24% to $48.52 on Tuesday, as oversupply concerns pushed oil prices down despite rising tensions in the Middle East,Reuters reports.

WTI crude is declining by 2.61% to $35.80 per barrel, while Brent crude is down by 2.50% to $36.29 per barrel this afternoon, according to the CNBC.com index.

"The markets keep falling because globally, we're still oversupplied," Frost & Sullivananalyst Carl Larry told Reuters. "But, the Middle East tensions still have people scared and they're not sure if they should continue going in and selling. Prices could jump very quickly."

Exclusive Look Inside: You see Jim Cramer on TV. Now, see where he invests his money. Check out his multi-million dollar portfolio and discover which stocks he is trading. Click here to see the holdings for 14-days FREE.

Shares of Anadarko Petroleum, based in The Woodlands, TX, gained about 1.4% to $49.80 before the market open this morning after the oil and gas production company was upgraded to "buy" from "neutral" at Citigroup, Barron's reports.

Recently, TheStreet Ratings objectively rated this stock according to its "risk-adjusted" total return prospect over a 12-month investment horizon. Not based on the news in any given day, the rating may differ from Jim Cramer's view or that of this articles's author. TheStreet Ratings has this to say about the recommendation:

We rate ANADARKO PETROLEUM CORP as a Sell with a ratings score of D. This is driven by several weaknesses, which we believe should have a greater impact than any strengths, and could make it more difficult for investors to achieve positive results compared to most of the stocks we cover. The company's weaknesses can be seen in multiple areas, such as its deteriorating net income, disappointing return on equity, poor profit margins, weak operating cash flow and generally high debt management risk.

Highlights from the analysis by TheStreet Ratings Team goes as follows:

- The company, on the basis of change in net income from the same quarter one year ago, has significantly underperformed when compared to that of the S&P 500 and the Oil, Gas & Consumable Fuels industry. The net income has significantly decreased by 305.6% when compared to the same quarter one year ago, falling from $1,087.00 million to -$2,235.00 million.

- Return on equity has greatly decreased when compared to its ROE from the same quarter one year prior. This is a signal of major weakness within the corporation. Compared to other companies in the Oil, Gas & Consumable Fuels industry and the overall market, ANADARKO PETROLEUM CORP's return on equity significantly trails that of both the industry average and the S&P 500.

- The gross profit margin for ANADARKO PETROLEUM CORP is rather low; currently it is at 23.45%. It has decreased significantly from the same period last year. Along with this, the net profit margin of -100.22% is significantly below that of the industry average.

- Net operating cash flow has significantly decreased to $1,127.00 million or 51.48% when compared to the same quarter last year. In addition, when comparing the cash generation rate to the industry average, the firm's growth is significantly lower.

- The debt-to-equity ratio of 1.13 is relatively high when compared with the industry average, suggesting a need for better debt level management. Even though the debt-to-equity ratio is weak, APC's quick ratio is somewhat strong at 1.02, demonstrating the ability to handle short-term liquidity needs.

Instablogs are blogs which are instantly set up and networked within the Seeking Alpha community. Instablog posts are not selected, edited or screened by Seeking Alpha editors, in contrast to contributors' articles.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a short position in APC over the next 72 hours. (More...)

Summary

Crude oil is still in bearish mood.

Anadarko should see further balance sheet strain.

The U.S. dollar is another drag.

Crude oil is still in bearish mood

Crude oil is still in bearish mood

In my weekly oil instablog, I warned of the bearish tone in crude oil as it failed to get above key resistance the last two weeks despite attempts from Saudi Arabia to talk the market up with some Draghi-esque comments of doing "whatever it takes" to see higher crude prices.

Failure to create any substantial follow-through was a worrying sign for the bulls and another hint that the market has given up on a rebound in crude in the near term, and the risks are still to the downside amidst growing supply in the market.

Anadarko should see further balance sheet strain

Now that oil has shown its cards with another drop towards $40, I am ready to initiate a short in Anadarko Petroleum (NYSE:APC).

Anadarko's recent third-quarter results saw the company report a disappointing headline net loss of $2.23bn, or $4.41 per share. As the price of crude makes another move to the downside, the chances of respite for oil companies looks slim and the company should suffer over the next 2-3 quarters.

APC ended the third quarter with only $2.1bn of cash on hand, which has eroded from $7.37bn at the end of 2014. The company currently holds long-term debt of almost $16bn, and this has developed despite a reduction of assets by $12bn.

Chairman, President and CEO Al Walker said the company, "continued our focus on maintaining long-term flexibility, while enhancing short-cycle returns by delivering higher-margin sales volumes for lower costs." Management has reigned in capex and looked for efficiencies, which would leave the company better positioned for a return to a growth environment. Unfortunately for Anadarko's executives, that environment was expected to have come to fruition by now, so as energy prices continue to weigh, APC is clearly being backed into a corner, alongside much of the industry as time catches up with the strategy of cost cutting and asset sales alongside higher production.

The U.S. dollar is another drag

Another weight on oil has been the rising U.S. dollar, and Janet Yellen has given a clear indication that the economy is now fit enough to handle a rise in interest rates.

As the situation in the Middle East deteriorates, and as emerging markets and Europe continue to see capital outflows, a rising yield on U.S. debt is likely to strengthen that trend, and it highlights the tough position that the Fed is now in. Raise rates too fast and capital flows will inflate prices. Raise them too slow and blow further bubbles in equity markets. The trends look to be on the side of further dollar gains, which will continue the pressure on crude amidst the ongoing supply glut.

Summary

Another push to the downside for oil should have investors considering the unthinkable - that a retest of the previous lows (and further) is once again possible and that the bearish trend could continue for another 3-6 months. Although Anadarko has abandoned a growth strategy, it is worrying that the cash position is deteriorating in a climate of higher production and cost cutting, meaning that now is not the time to get in. I am going short Anadarko with a target of $40.

Aucun commentaire:

Enregistrer un commentaire